Wall Street slumped Monday as rising yields cranked up the pressure.

CLOSING BELL

Wall Street slumped Monday as rising yields cranked up the pressure.

The renewal comes amid strong ratings for Season 6. The Alexi Hawley-created crime drama starring Nathan Fillion kicked off its sixth season with its most-watched episode in nearly six years, with 11.92 million total viewers across platforms after 35 days of viewing. That's up 14% from its Season 5 average and marks the show’s strongest MP35 number since Oct. 23, 2018, according to the network and Nielsen.

Five years after parting ways with the Disney-ABC Television Group, Ben Sherwood is getting back in the media game. The one-time ABC News president has been granted a minority stake in The Daily Beast, the news and opinion site created by Tina Brown in 2008 an owned by Barry Diller's IAC Inc.

CBS just announced that the network will rebroadcast Billy Joel: The 100th – Live at Madison Square Garden special in its entirety this Friday, April 19, after Sunday’s presentation cut out in some parts of the country as the singer was in the middle of his signature hit Piano Man. The special will be rebroadcast in its entirety on CBS on April 19 at 9 p.m. ET/PT.

The agreement with Scripps News will allow for Ad Fontes to undertake a more granular audit of content across Scripps News’ TV and digital news portfolio using Ad Fontes’ proprietary, two-tiered system.

Massive levels of linear TV programming on CTV platforms (connected TV) have resulted by making up around 85% of total CTV ad inventory for long-form content, according to Bernstein Research. The stock research firm expects CTV ad inventory to end up growing 3% in the first quarter of this year, with linear inventory sinking 6% year-over-year.

"I have loved working with you and something tells me Charles, this will not be the last time that we're working together," Gayle King told Charles Barkley in what was the show's final episode.

The study will explore innovations in measurement, currency, data and metrics across the local TV and video marketplace.

Suits will make its broadcast television debut on MyNetwork TV this fall, where it will be offered on free television for the first time. The legal drama, created and written […]

The new product using ATSC 3.0 “introduces personalization, hyper-localization and enhanced content capabilities to broadcast TV. Digital features advance viewer experience and enable increased engagement, advertising and measurement opportunities.” It’s now available on select NBC- and Telemundo-owned stations and is being showcased at this week’s NAB Show.

Picking up Disney’s second longest-running syndicated show are ABC Owned Television Stations and leading broadcast groups including Hearst, Scripps, Nexstar, Tegna, Gray and Allen Media Group.

A new consumer research study reports that 50% of video-viewing households now use FAST services weekly.

The flow of traffic to Donald Trump’s most loyal digital-media boosters isn’t just slowing; it’s utterly collapsing.

ROXi’s FastStream technology allows local TV news organizations to create interactive versions of their broadcast TV news where viewers can pause, play and skip news segments instantly without need to download an app. The new format is designed to make broadcast TV compelling and attractive to younger consumers and build demand for NextGen TV devices.

Wall Street titan Mario Gabelli is slamming a possible merger between Paramount and Skydance Media — and says he’d rather see Paramount exit deal talks altogether. The legendary investor — whose firm through super voting shares and common Paramount stock is the second leading voting shareholder next to media heiress Shari Redstone — added in an interview with the New York Post that he’s also against a sale of Paramount to Apollo Global Management, which has offered $26 billion. (Scott Mlyn/CNBC)

J.P. Morgan and Morgan Stanley started coverage on Reddit with equivalent to "hold" ratings, as they wait for clarity on the social media company's user growth, while staying bullish on ad-revenue growth and artificial intelligence (AI) initiatives. Shares of Reddit were up 0.88% at $42.64 in premarket trading. While Reddit, which made its market debut last month, still relies on advertising for the vast majority of its revenue, it touted AI in its initial public offering marketing roadshow as an area of growth.

Dan Lin, the streaming service’s new film chief, wants to produce a more varied slate of movies to better appeal to the array of interests among subscribers.

The Ultimate Fighting Championship, whose 300th numbered pay-per-view fight card was last weekend, was once effectively banned on television because of its violence.

Brands want to measure ads everywhere, but media companies keep making it harder.

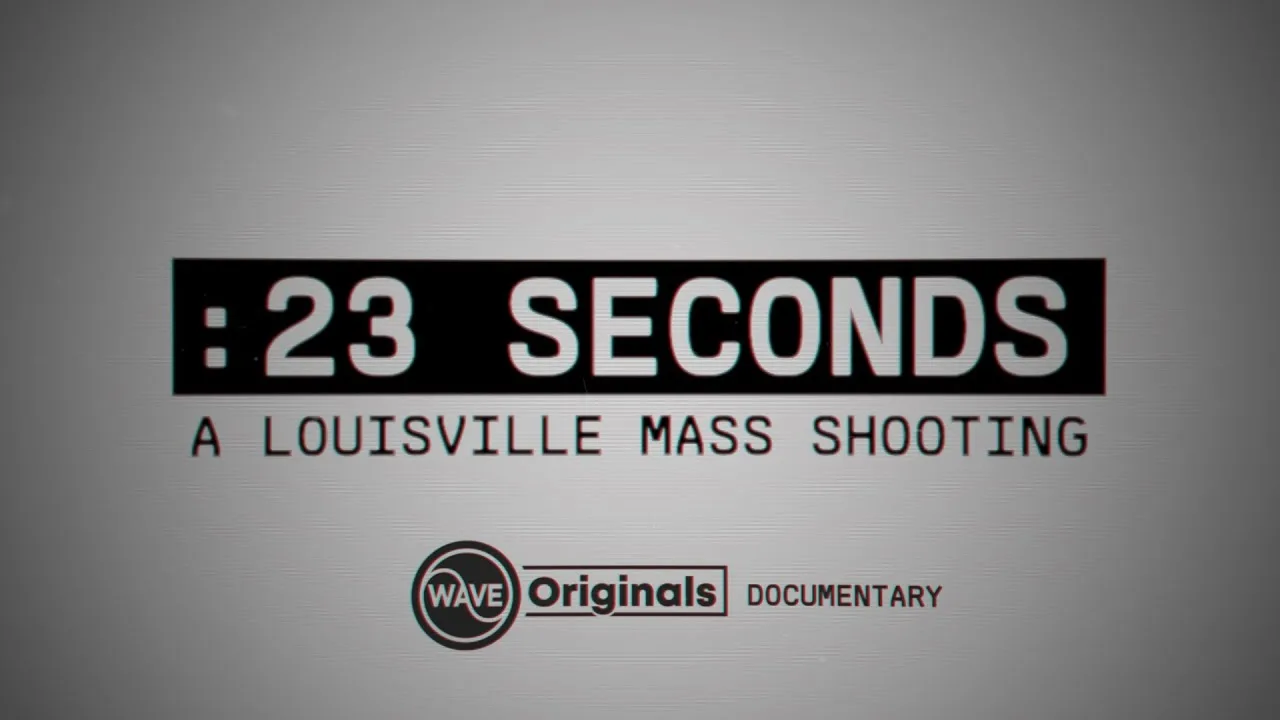

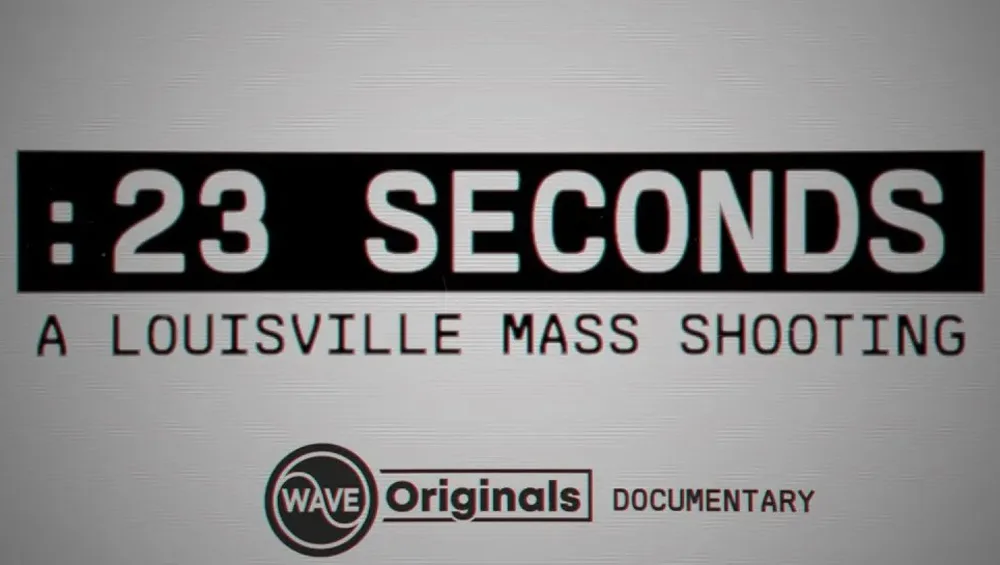

Natalia Martinez, WAVE’s investigative reporter who executive produced the documentary, says “the response has been overwhelming. Viewers sent us messages and emails and called the station.” She says the volume of responses is unlike anything the station has seen.

New jobs posted to TVNewsCheck’s Media Job Center include an opening for an account executive – trainee/new business development and existing jobs include 13 openings in news, sales, digital and engineering.

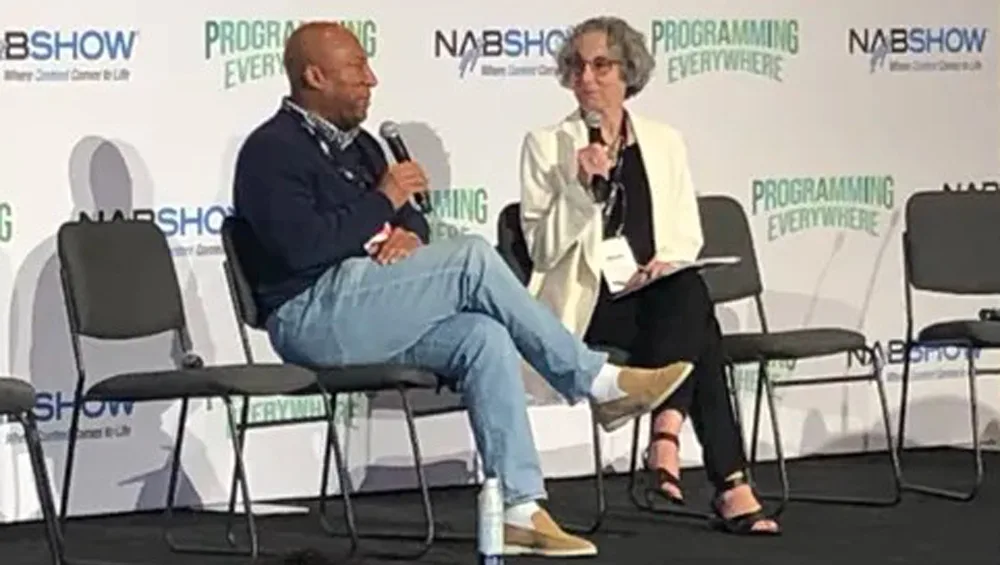

Byron Allen, founder, chairman and CEO of Allen Media Group, spoke about his bid to acquire Paramount Global at NAB Show April 14. Allen called Paramount Global “a phenomenal company” and a healthy one at that. Allen was interviewed on a panel titled “Thriving in a New Television Syndication Paradigm” by Kathy Haley, publisher of TVNewsCheck. Allen said he would pursue a streaming merger with the likes of NBCUniversal’s Peacock and Warner Bros. Discovery if he were to acquire Paramount. “I think there will be a shakeout; I think there will be some merging,” he said of the various streamers. (Michael Malone)

ABC, CBS, CNN, Fox, PBS, NBC, NPR and The Associated Press are among those that signed on to the letter urging presumptive presidential nominees Joe Biden and Donald Trump to agree to debates this year.

The Iowa native delivered a heartfelt message about her basketball future, thanking many of the great players who came before her. "I'm sure it will be a big first step for me, but it's just one step for the WNBA thanks to all the great players like Sheryl Swoopes, Lisa Leslie, Cynthia Cooper, the great Dawn Staley, and my basketball hero, Maya Moore," Clark said. "These are the women that kicked down the door so I could walk inside. So, I want to thank them tonight for laying the foundation. Clark came back on stage at the end of the show, bringing her former Hawkeye teammates Kate Martin, Gabbie Marshall and Jada Gyamfi with her. (Chrlaie Neibergal/AP)

Many in the veteran genre are introducing apps, QR codes, the metaverse and more to retain and engage audiences, grow viewers and optimize monetization.

Content delivery network Edgio is the first partner for these new data offloading capabilities.

With NextGen TV broadcasts now within reach of more than 240 million Americans and sales of televisions and upgrade accessory devices expected to top 5 million units this year (according to the Consumer Technology Association), local TV broadcasters transmitting in NextGen TV are ramping up to support High Dynamic Range (HDR) video and immersive audio as an “always on” viewer benefit.

McManus, who turned 69 in February, started to consider retirement two years ago. With CBS carrying the Super Bowl this year along with the NCAA Tournament and the Masters, McManus and CBS President-CEO George Cheeks agreed the timing was right. David Berson, president of CBS Sports for over 10 years, is McManus' hand-picked successor.

Streaming sales leaders from Gray Television, E.W. Scripps, Hearst Television and Ticker will share the latest developments in technology and strategy for OTT and FAST channels. Learn more about this critically important revenue source for broadcasters in a TVNewsCheck Working Lunch Webinar on May 16. Register here.

Morris Multimedia’s WWAY Wilmington secured Center for Quality Care as an interactive sponsor for its Weather Photo of the Day user-generated content (UGC) segment. Sponsored UGC segments can be a great source of revenue for local broadcasters and an excellent opportunity for brands looking to drive instant leads and sales.

16 May 2024

23 May 2024